Strategic Management Accounting that creates change resilience and enhances financial strength and profitability

It has been one year and three months since WHO recognized the new coronavirus as a pandemic on March 11, 2020. The infection of the new coronavirus has spread all over the world, and the social and economic conditions of the globalized world have been severely damaged, and its vulnerabilities have been highlighted.

New management issues that have become apparent due to the COVID-19

-Deterioration of break-even point due to decrease in sales

-Expanding the gap between management and on-site awareness due to the impact of the COVID-19

-Increasing number of internal frauds, fraudulent accounting of overseas subsidiaries, and inadequate internal control

-Roadmap, goal setting and concrete measures for the realization of a carbon-free society

Under these circumstances, what is most needed is the ability to respond to change by making use of hypotheses and verifications, in addition to the wisdom accumulated in the past, such as failure experiences and success experiences.

In order to build a corporate structure that responds to change, it is necessary to manage change points by narrowing the pitch rather than managing goals. To that end, it is urgent to align the common operation cycle weekly, chain conventional management indicators (financial indicators and non-financial indicators), and manage the cockpit with the idea of the Balanced Scorecard.

Cash is King

After the unprecedented financial crisis Lehman shock on September 15, 2008 and the Great East Japan Earthquake on March 11, 2011, WHO has announced the new coronavirus was equivalent to a pandemic (a global epidemic) on March 11, 2020.

The era of VUCA (since the 2010s)

VUCA is an acronym made from Volatility, Uncertainty, Complexity, Ambiguity, and represents the modern chaotic economic environment. In other words, it means "unpredictable state". In addition, global warming and environmental issues are the most important and urgent issues for ESG and SDGs.

Under these circumstances, what is most needed is the ability to respond to change by making use of the wisdom from past failed experiences and successful experiences.

In order to build a corporate structure that can respond to changes, it is necessary to manage the points of change with a narrower pitch than target management.

To that end, it is an urgent task to align common operation cycles on a weekly basis, chain conventional management indicators (financial indicators and non-financial indicators), and carry out cockpit management with the idea of a balanced scorecard.

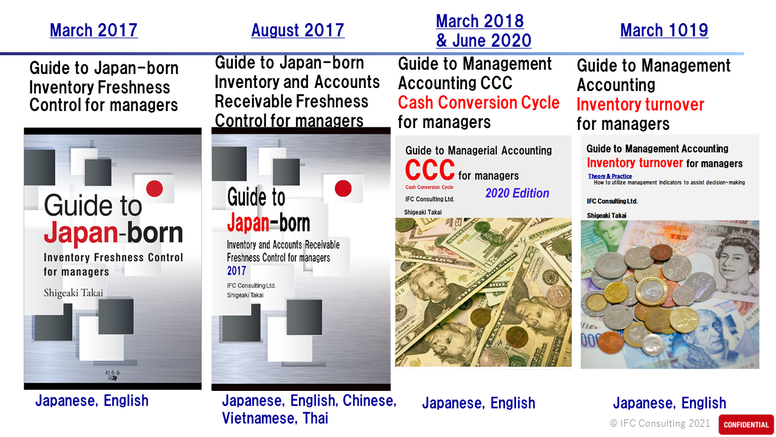

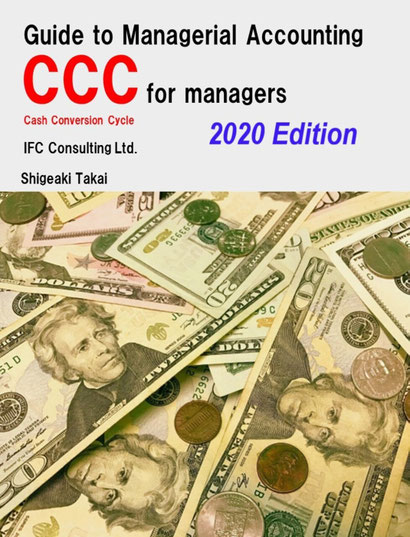

This book explains CCC by comparing it with Japan, the US, and Europe using the latest quarterly financial results figures (end of March 2020) that can be grasped at the time of publication. This is a must-have book for business owners as a guide to improving asset efficiency.

ROE (Return on Equity) has been gradually improving in Japan and is drawing attention now.

According to the Ito report announced by the Ministry of Economy, Trade and Industry in August 2014, it was pointed out that the issues of Japanese companies are not in asset turnover rates and financial leverage, but in terms of their ability to make earnings, compared to western companies. However, I believe that both accounts receivable turnover and inventory turnover are generally lower than those in Europe and the United States, among asset turnover rates, which is an issue for CCC (Cash Conversion Cycle) management.

As for inventory, we position inventory turnover days as company-wide common control index for decision-making, not traditional inventory turnover rate and inventory turnover period, and we propose integrated activities of management team and operation site to improve ROE and ROIC (Return on Invested Capital).

Inventory is an important management resource

Inventory is said to be a source of profit for business, at the same time, to cause loss. Especially in manufacturing, retail and wholesale business, management indicators are used to measure whether product inventory is being converted into sales efficiently.

In general, the following two indicators are used.

1. Inventory turnover rate

Inventory turnover = sales · cost of sales (annual) ÷ inventory amount

The inventory turnover rate is mainly used by executives for presentations for investors or shareholders.

2. Inventory turnover period

The inventory turnover period is an indicator that shows how long it takes to have inventory for days or months, or to consume (sell) all inventory.

Inventory turnover period = inventory amount ÷ sales or cost of sales (monthly or daily)

Both are said to be indicators to see if inventory is appropriate. It is enough to tell about past and current situation of inventory, but I think that it is inappropriate as an indicator for future decision making. In other words, it is an index for financial accounting, not inventory turnover as management accounting.

As an Inventory-centric management consultant, I am convinced that inventory turnover period is an indicator that can assist decision-making to be shared by management, operations staffs such as sales, manufacturing, procurement and logistics.

Rather than handling inventory turnover as a mere indicator used at the operation site, in order to create corporate value, in relation to other management indicators as management accounting, and also in order to effectively encourage the improvement activities, what kind of practical knowledge, the systems which supports and finally practical solutions and concrete examples for inventory management through my vast experience accumulated are explained.

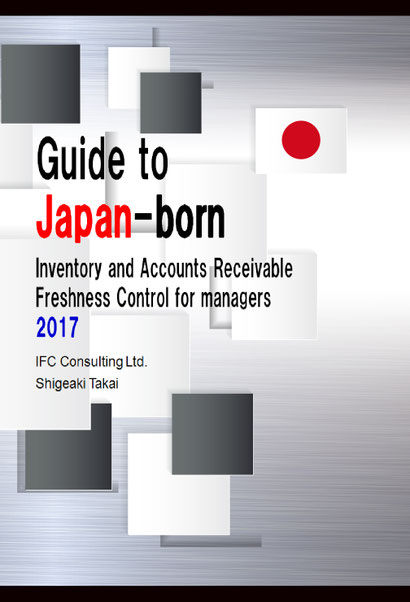

In this book, I have explained CCC using the latest quarterly settlement of accounts figures (as of the end of January 2019) that can be grasped at the time of publication which also different from conventional books.

It would be greatly appreciated if it could be utilized as a guide book for inventory control.

The proper Inventory and Accounts Receivable control can solve all management issues!

Having engaged in production and distribution for many years at Sony and familiar with "inventory management" of domestic and foreign companies, author explains as to what is Inventory-centric management consulting.

While inventory is the fountainhead of profits for business, it also brings about a loss and is only a result of operation.

Focusing on three issues related to inventory (① Increase in working capital ② Increase in disposal costs ③ Reduction of accounting fraud risks), the essence of inventory management is clearly explained, that is freshness (time-axis) management of goods and thorough weekly operation.

Case studies of domestic major companies acquired through interview, Cash Conversion Cycle between Japan and US is thoroughly compared. Also, referring to the latest world food problem, advocating to suppress overproduction and excess supply. Following the English translation version, the book will be published in multiple languages to promote inventory freshness control.

Manufacturing, logistics, food · · · Management executives, Corporate control staff, SCM person responsible person for all industries must read.

The data has been updated for 2017.

Reference book on mitigation of overproduction and accounting fraud risks The proper Inventory and Accounts Receivable control can solve all management issues! Having engaged in production and distribution for many years at Sony and familiar with "inventory management" of domestic and foreign companies, author explains as to what is Inventory-centric management consulting. While inventory is the fountainhead of profits for business, it also brings about a loss and is only a result of operation. Focusing on three issues related to inventory (① Increase in working capital ② Increase in disposal costs ③ Reduction of accounting fraud risks), the essence of inventory management is clearly explained, that is freshness (time-axis) management of goods and thorough weekly operation. Case studies of domestic major companies acquired through interview, Cash Conversion Cycle between Japan and US is thoroughly compared. Also, referring to the latest world food problem, advocating to suppress overproduction and excess supply. Following the English translation version, the book will be published in multiple languages to promote inventory freshness control. Manufacturing, logistics, food · · · Management executives, Corporate control staff, SCM person responsible person for all industries must read.

Guide to Japan-born Inventory Freshness Control for managers (for printed book)

While inventory is the fountainhead of profits for business, it also brings about a loss and is only a result of operation.

Focusing on three issues related to inventory (① Increase in working capital ② Increase in disposal costs ③Reduction of accounting fraud risks), the essence of inventory management is clearly explained, that is freshness (time-axis) management of goods and thorough weekly operation.

Case studies of domestic major companies acquired through interview, Cash Conversion Cycle between Japan and US is thoroughly compared. Also, referring to the latest world food problem, advocating to suppress overproduction and excess supply. Following the English translation version, the book will be published in multiple languages to promote inventory freshness control.

Manufacturing, logistics, food · · · Management executives, Corporate control staff, SCM person responsible person for all industries must read.